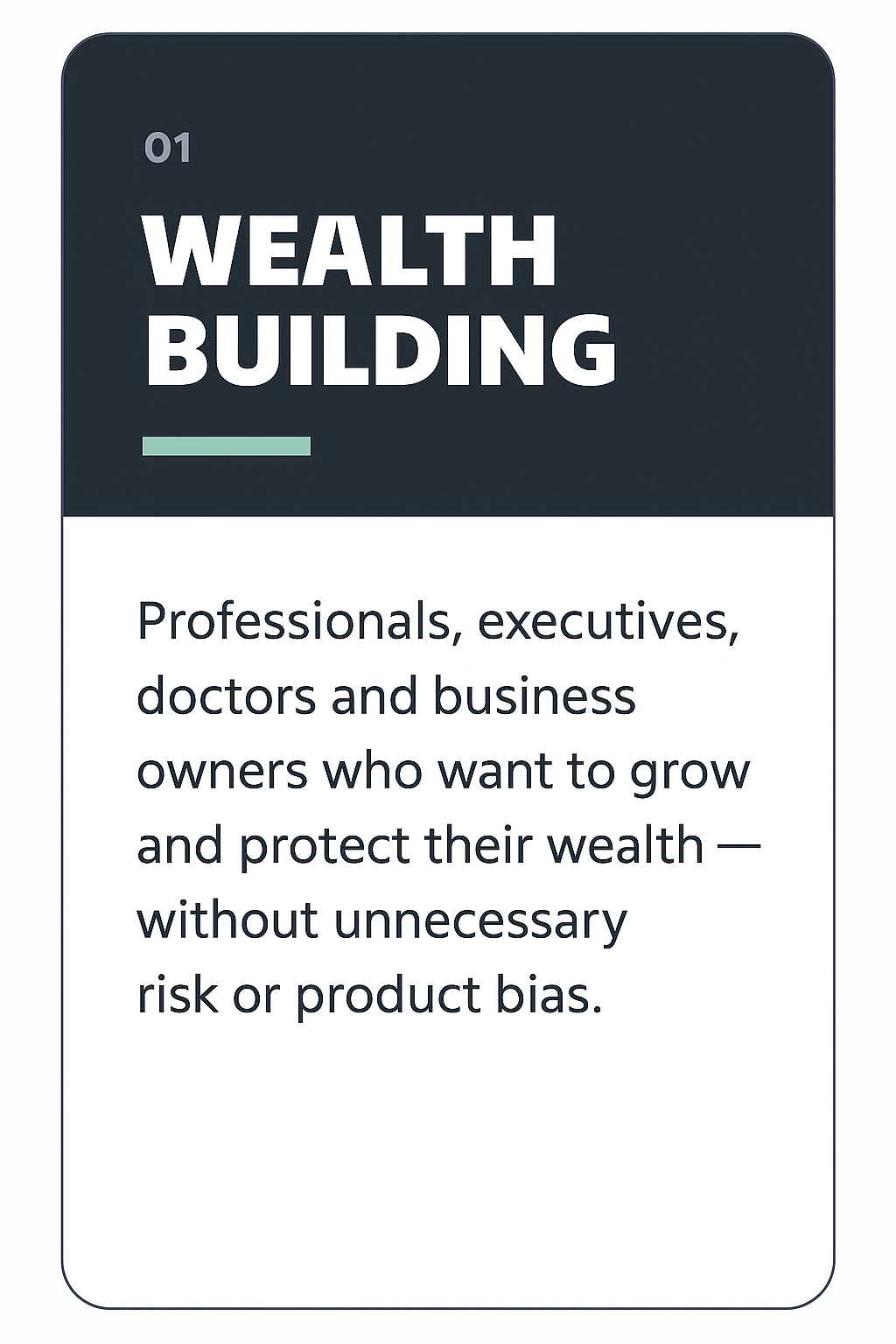

Wealth builders we work with generally have:

🎯a household income of more than $300,000

🎯are able to save more than $3,000 a month

🎯more than $500,000 in investments (including super)

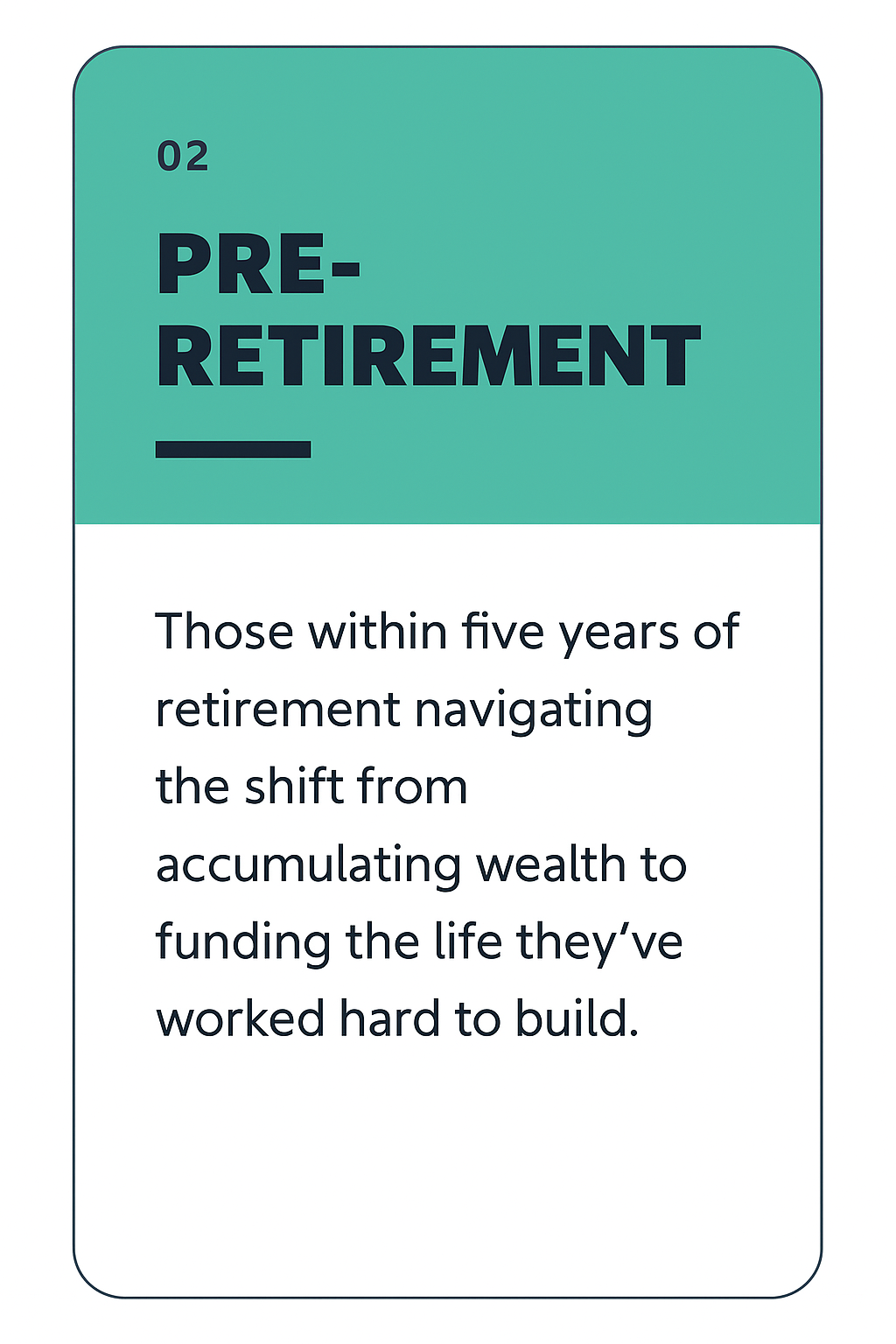

Pre-retirees that we work with generally have

- a household income of more than $300,000

- are able to save more than $2,000 a month

- more than $750,000 in investments (including super)

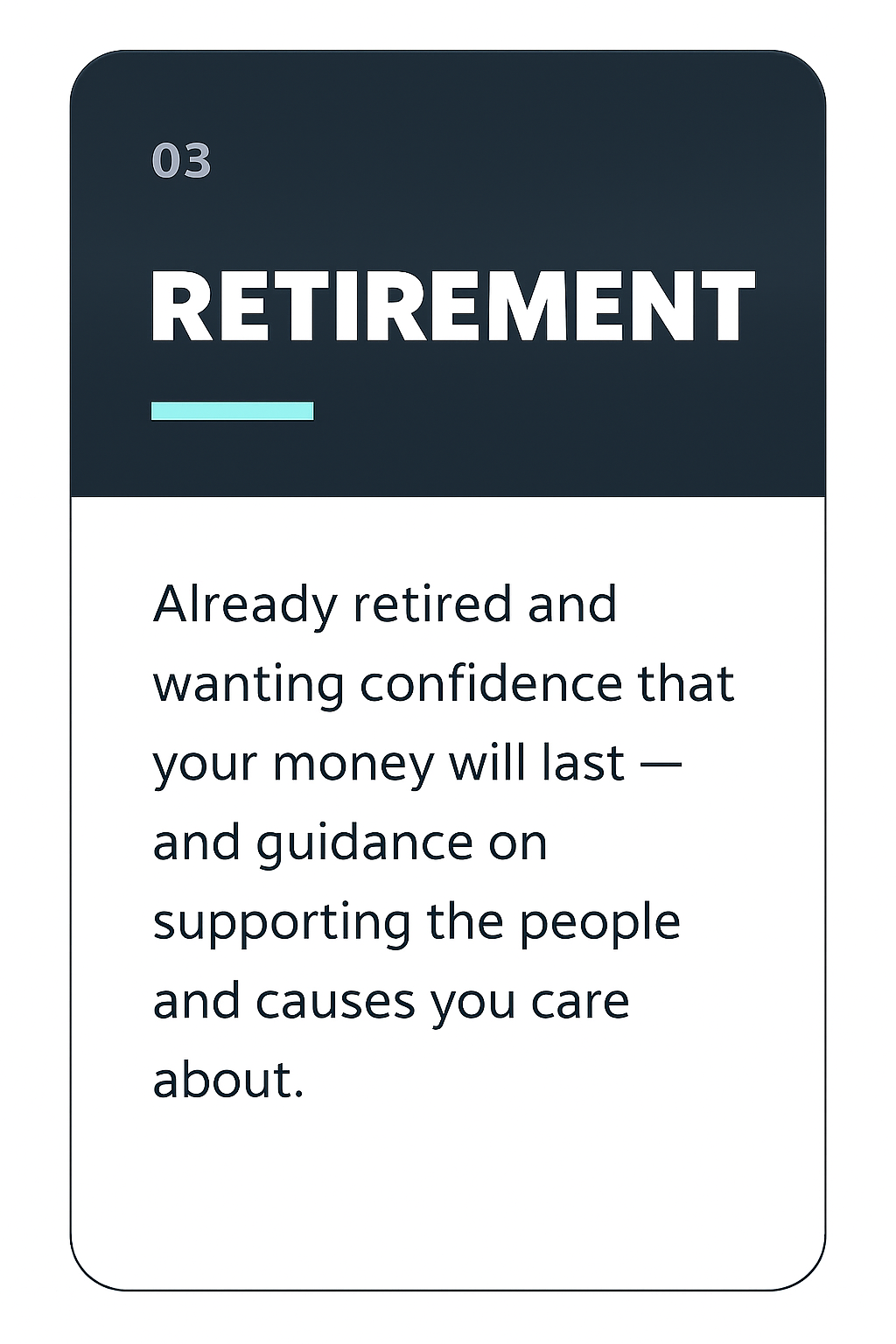

Retirees that we work with generally have

- more than $1 million in investments (including super)

Case study 1 – Came to us wanting direction, gave them a plan to save $150k in tax

Background

- Married couple in their late 40’s with two kids

- He is an executive and she is an admin assistant. Combined income of more than $400,000

- Like many people in similar positions they had followed the path of buy your first home, pay it off and save the deposit for an investment property ➡️ buy an investment property, pay it off and save the deposit for the next one ➡️buy another investment property, pay it off and save the deposit for the next one.

- They were now at the point where they had saved enough for the deposit for the third one.

- Everything else was going well. Good incomes, healthy super balances, kids just about to leave home, all the usual things.

The problems we saw

1️⃣ They bought units that weren’t going to provide long-term capital growth

2️⃣ The net rental yield (ie after body corporate, land tax, insurance, etc) was only about 2.5%. Hint, it’s not a great idea to buy units with a net yield of <3% if capital growth is only around 3-4%.

3️⃣ There was no debt against the investment properties and it was held in the name of the highest income earner – this meant the income was being taxed at 47%.

What we recommended

❌Sell one of the investment properties.

❌Buy the next property (which is being purchased for family purposes, but will be rented out) with 105% debt in the name of the highest income earner.

❌Use their savings to make super contributions.

❌Invest future savings through super.

The outcome

💲They will save $4,000 a year on unnecessary insurance premiums

💲Over the next ten years they will save more than $150,000 in tax

💲Their wealth is projected to be more than $400,000 higher in ten years than it was going to be

Case study 2 – Retire at 55

Background

- Married with three kids

- Late 30’s

- Blue collar workers with a combined income of $160,000

- Both have super ($150,000 combined) through one of Australia’s largest Industry super funds which boasts low fees as one of the reasons you should switch to them

- Their employers contribute 9.5% to super

- Have a mortgage of around $500,000

Outcome

- They have a plan to be able to retire by the time they are 55

- They can continue going on regular family camping trips and creating memories with their kids

- They have a plan to save for their kids’ education

- Changing super funds means that between them they will be saving more than $120,000 in fees

- Their super is now invested in a diversified portfolio that will give them returns that are better than 75% of similar investments

- They are saving $1,800 a year in insurance premiums (and for superior insurance) compared to what they would have been paying through their super fund.